JAIN SWASTHYA BIMA YOJANA RENEWAL / NEW POLICY (2022-2023)

We have Renewed JIO Mediclaim Policy and New Policy Offer .Policy Insured by Universal Sompo General Insurance And Servicing by Gallagher Insurance Brokers Private Limited

Scheme Enrollment Closed on 19-04-2022

JAIN SWASTHYA BIMA YOJANA RENEWAL / NEW POLICY (2022/2023)

PARTNERS for JIO MEDICLAIM POLICY

Insurance Company: Universal Sompo General insurance Co. Ltd.

TPA: Ericson Insurance TPA Pvt. Ltd.

Insurance Brokers: Gallagher Insurance Brokers Private Limited & Synergy Insurance Broking Services Pvt. Ltd.

Policy Period: 20th April, 2022 to 31st March, 2023. Since you have paid after expiry of your policy on 31st March, 2022, during enrolment extension time, your cover shall start from 20th April, 2022 and No Claim Shall be allowed / considered if hospitalisation falling between 1st April, 2022 to 19th April, 2022. However, renewal member will get continuity benefit for hospitalisation after 20th April, 2022.

- FAMILY DEFINITION: (1+7) maximum 8 members: Primary Member + Spouse + 4 Dependent, Unmarried children up to 25 years of age + Parents or Parents in law. (Any one set of parents only allowed). All members have to be Jain only.

Policy premium Details for Mediclaim Policy RENEWAL or NEW POLICY (2022-2023).

|

Family Size |

Sum Insured |

Premium Amount (With GST) 0-45 Y rs. |

Premium Amount (With GST) 46-60 Yrs. |

Premium Amount (With GST) 61-90 Yrs. |

|

Individual (only for Renewal members who had 2 Lac individual SI last year under same policy plan) |

Rs. 2 Lakh |

8,000 |

8,000 |

8,000 |

|

Family Floater of size 1+7 |

Rs. 2 Lakh |

15,000 |

20,000 |

30,200 |

|

Family Floater of size 1+7 |

Rs.6 Lakh |

21,000 |

30,000 |

44,500 |

|

Family Floater of size 1+7 |

Rs.10 Lakh |

30,000 |

38,000 |

63,300 |

· Room Rent : Room Rent limitation Per Day will be as below:

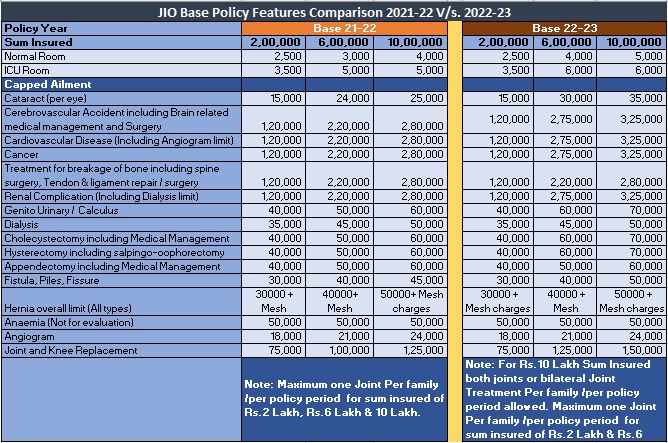

|

Sum Insured |

Per Day Limit (Inclusive of Nursing, RMO, BMW, Infection control charges etc.) |

|

|

Normal Room |

ICU |

|

|

200,000 |

2,500 |

3,500 |

|

600,000 |

4000 |

6000 |

|

10,00,000 |

5,000 |

6,000 |

|

**IF THE INSURED OCCUPIES A ROOM WITH A ROOM RENT LIMIT OTHER THAN HIS ELIGIBILITY AS PER THE INSURANCE POLICY, THEN ALL THE OTHER CHARGES SHALL BE LIMITED TO THE CHARGES APPLICABLE FOR THE ELIGIBLE ROOM RENT OR ACTUALS, WHICHEVER IS LOWER** |

||

We recommend you to also enrol for Super top up policy to avoid deduction on account of capping in base policy. For e.g. In 10 lac policy there is capping of Rs. 2.80 Lakh for Cardiovascular disease. If you enrol in Super top up policy with deductible of Rs. 3 Lakh with SI of Rs. 10 Lakh, you can claim balance amount above 3 Lakh from the Super top up policy.

PLEASE NOTE:

- Corona Virus disease treatment is covered under the policy as per Terms & Conditions.

- The above plan covers Personal Accident cover for Rs.5,00,000/- per person for each covered member of the family between the age of 18 years to 75 years of age. So, in a family if there are 6 members than total Rs.30,00,000/- sum insured is available under the above plan. Nominee of the member will be spouse in case of married proposer's death and in case of unmarried proposer death, father or mother will be nominee.

- Member can increase the Sum Insured during renewal, But can't decrease it.

- No Changes or cancellation are allowed in the policy once the payment is done.

- The policy premium will be paid directly by the member to USGIC account through payment gateway. USGIC will get consolidated premium through single remittance by the payment gateway. All the members will get Certificate of Insurance for the premium paid by him/her.

- Policy Premium can be PAID only via Online Payment. CHEQUE / NEFT / RTGS will not be accepted.

- Elderly Care benefit above 60 Years aged people who would be hospitalized given for 60 days post discharge.

- Additional amount will be charged by payment gateway (PayU) for providing safe & secure online money transfer facility, which is addition to above Policy Premium charges.

Payment gateway Convenience fees (+18% GST on Convenience Fees)

|

Payment Modes |

Convenience fees (GST extra) |

|

Debit Card (Visa, Master, Rupay, Maestro, etc.) |

Rs. 20 |

|

Debit card (Visa, Master, Rupay, Maestro, etc.) Above 2000 Rs. |

Rs. 20 |

|

Credit Card(Visa, Master, Rupay, Maestro, etc.) |

0.87 % |

|

Net Banking |

Rs 15 |

|

UPI (G-Tez, Phone Pe, etc.) |

Rs 15 |

- JIO JAC membership fees (non-refundable / non-transferable) for the financial year 21-22 is Rs. 1000 (GST extra) same is additional to above Policy Premium. (Payment will get updated in next 1 week)

- GST refund certificate will not be available under this policy however 80-D certificate under Income Tax will be provided in the name of proposer in the policy.

|

Scope of Coverage: |

2022-23 |

|

1) Cashless & Reimbursement Facility |

Member can avail BOTH CASHLESS facility as well as REIMBURSEMENT facility. |

|

In case of cashless claims, immediate intimation shall be given to our Call Centre within 48 hours of Hospitalization. In case of reimbursement claims, immediate intimation shall be given to Call Centre within 48 hours of Hospitalization. Toll Free Number : 18002022034 / 022-41548300. Email - jiointimation@ericsontpa.com |

|

|

2) Corona Virus COVID-19 Cover |

Corona Virus Treatment is covered under this policy. Subject to tested positive in government authorized lab. Home quarantine treatment is not covered. |

|

3) Reimbursement |

Available with mandatory 48 Hrs intimation (Toll Free Number : 18002022034 / 022-41548300. Email - jiointimation@ericsontpa.com ) |

|

4) Claim Intimation |

In case of Cashless Claims, immediate intimation would be given on Toll Free Number : 18002022034 / 022-41548300 within 48 hours of Hospitalization or before discharge, whichever is earlier. In case of Reimbursement Claims, immediate intimation shall be given to Call Centre within 48 hours of Hospitalization. |

CAPPINGS 2022-23 This limit is overall limit, including Pre/post claim

|

Sum Insured |

2 Lacs |

6 Lacs |

10 Lacs |

|

Cataract (per eye) |

15,000 |

30,000 |

35,000 |

|

Cerebrovascular Accident including Brain related medical management and Surgery |

1,20,000 |

2,75,000 |

3,25,000 |

|

Cardiovascular Disease (Including Angiogram limit) |

1,20,000 |

2,75,000 |

3,25,000 |

|

Cancer |

1,20,000 |

2,75,000 |

3,25,000 |

|

Treatment for breakage of bone including spine surgery, Tendon & ligament repair / surgery |

1,20,000 |

2,20,000 |

2,80,000 |

|

Renal Complication (Including Dialysis limit) |

1,20,000 |

2,75,000 |

3,25,000 |

|

Genito Urinary / Calculus |

40,000 |

60,000 |

70,000 |

|

Dialysis |

35,000 |

45,000 |

50,000 |

|

Cholecystectomy including Medical Management |

40,000 |

60,000 |

70,000 |

|

Hysterectomy including salpingo-oophorectomy |

40,000 |

60,000 |

70,000 |

|

Appendectomy including Medical Management |

40,000 |

50,000 |

60,000 |

|

Fistula, Piles, Fissure |

30,000 |

40,000 |

50,000 |

|

Hernia overall limit (All types) |

30,000 |

40,000 |

50,000 |

|

Anaemia (Not for evaluation) |

50,000 |

50,000 |

50,000 |

|

Angiogram |

18,000 |

21,000 |

24,000 |

|

Joint and Knee Replacement |

75,000 |

1,25,000 |

1,50,000 |

|

maximum one Joint Per family /per policy period for sum insured of Rs.2 Lakh & Rs.6 Lakh.

For Rs.10 Lakh Sum Insured both joints or bilateral Joint Treatment Per family /per policy period allowed. |

* Compulsory deduction of Rs. 5000 will be applicable for each & every claim (applicable also in capped ailment listed above).

**Joint replacement capping will be applicable even if cause of Joint replacement is fracture.

We are happy to announce that the existing ELDERLY MEMBERS covered under the Policy who have already completed 90 years of age, are welcome to continue the cover in the Renewal for lifetime.

- FAMILY FLOATER MEDICLAIM: Sum Insured of Rs.2 Lacs, Rs.6 Lacs and Rs.10 Lacs.

- FAMILY DEFINITION: (1+7) maximum 8 members: Primary Member + Spouse + 4 Dependent, Unmarried children up to 25 years of age + Parents or Parents in law. (Any one set of parents only allowed). All members have to be Jain only.

- INDIVIDUAL POLICY with Sum Insured of Rs.2 Lacs can only be opted by members who were covered last year under individual policy (Widow or widower) who do not have live spouse, children, parent or parent in law.

- Any person cannot be covered in multiple family policy. If found enrolled in more than one policy, claim will be paid under one policy Sum Insured only during the whole year.

- Claim Intimation In case of Cashless claims, immediate intimation shall be given on Toll Free Number : 18002022034 / 022-41548300 within 48 hours of hospitalization. In case of Reimbursement claims, immediate intimation shall be given to Call Centre within 48 hours of hospitalization. You can also send claim intimation mail to jiointimation@ericsontpa.com

- PRE-EXISTING DISEASES are covered from Day One subject to 25% Co-payment.( any disease which is incepted prior to 1st April 2022 shall be consider as PED and 25% CoPay shall get deducted)

- CO PAYMENT:

- 25% co-pay ONLY on all PED claims. ( any disease which is incepted prior to 1st April 2022 shall be consider as PED and 25% CoPay shall get deducted)

- No co-pay will applied on Non-PED Cases.

- NO MEDICAL CHECK-UP required

- AGE LIMIT: 0-90 years Entry Age of Proposer Between 18 to 90 Years

10. Joint Replacement or Knee Replacement (including pre & post exp.) : covered subject to maximum one Joint Per family /per policy period for sum insured of Rs.2 Lakh & Rs.6 Lakh.

For Rs.10 Lakh Sum Insured both joints or bilateral Joint Treatment Per family /per policy period allowed.

- 2 Lac Sum Insured: Rs. 75,000 per family per policy year.

- 6 Lac Sum Insured: Rs 125,000 per family per policy year.

- 10 Lac Sum Insured: Rs 150,000 per family per policy year.

#Note

There will be ONE YEAR waiting period for Joint Replacement & Knee Replacement for New Members.

In case of ROAD TRAFFIC ACCIDENT the second joint replacement is covered. (Police FIR is MANDATORY) with above mentioned capping.

- Maternity benefits, applicable only for the Member or Dependent Spouse, subject to a limit of Rs.30, 000/- for normal and Rs.40, 000/- for caesarean delivery up to 2 live children only. Maternity is not covered in individual policy. Pre / Post claim is not allowed under Maternity claim.

- Maternity waiting period of 9 months for maternity waived off for all renewal members (2021-2022 Policy); however waiting period of 9 months is applicable for new members enrolled under this policy. Maternity is not covered in individual policy.

- No addition or deletion of members are allowed during policy period, except for New born child in the family or newly married spouse, subject to intimation received in mail on jio. insurance@edelweissfin.com within 20 days of marriage or birth (for newly married SPOUSE & new born BABY) coverage will start from date of birth / Marriage. However, claim of New-Born Baby will be processed under reimbursement basis only.

Mid-term addition is not allowed in the policy. Any changes with relation to name, date of birth, age & sex of members informed after date of hospitalisation will not be corrected by Insurance Company. Hence any correction with regards to same has to be informed to jio.insurance@edelweissfin.com within 5 days of payment. Post loss corrections/ endorsement is also not allowed.

- AYUSH Treatment Covered subject to the treatment being taken in a Government hospital or in any institute recognized by Government and/or accredited by Quality Council of India or National Accreditation Board on Health.

- Cyberknife, Cochlear Implant, and Psychiatric Treatment: Cyberknife and Cochlear implant covered with 50% co-payment and Psychiatric treatment covered upto Rs.30,000.

- Dental Treatment : covered if due to Road accident only and requiring 24 hours Hospitalisation (Police FIR compulsory).

- DAY CARE PROCEDURES: Day care procedures covered as per IRDA list.

- Emergency Ambulance Charges Covered maximum upto Rs. 2500/- per hospitalisation.

- Pre-Post Hospitalization Expenses (30/60 days respectively) Covered within Family Floater Sum Insured. Capping limit is including pre/post limit. Pre / Post claim is not allowed under Maternity claim .

- Internal Congenital Ailments Covered

- Compulsory deduction of Rs. 5000 will be applicable for each & every claim (applicable also in capped ailment listed above).

- Organ transplant: Donor Expenses for organ transplantation where the insured person is the recipient are payable provided the claim for transplantation is payable and subject to the liability of the sum insured. Donor screening expenses and Post-donation complications of the donor are not payable. Donor expenses cover is subject to limit of 10% of the Sum insured or Rs. One Lakh whichever is less.

- All JIO members who were associated with JIO Group Mediclaim Policy since year 2014 or any year after that but discontinued in any of the year can also avail the benefit of above policy by enrolling their family in 2022-2023 as a new member.

- Corona Virus Cover Treatment of COVID-19 is covered under policy even though it will be declared as Epidemic and/or Pandemic. However vaccination charges are not covered. Home quarantine treatment is not covered.

- Shravak Arogyam Personal Accident Policy (GPA cover)

Group Personal Accident cover is also offered to all family members covered in the mediclaim policy, in case of Accidental Death for sum insured of Rs.5,00,000/- irrespective of his sum insured under mediclaim policy. Police FIR is compulsory for all PA claims.

The personal Accident benefit is extended to all family members covered in mediclaim policy. The family member for this benefit to avail should be within 18 years to 75 years of age at the time of enrolment.

This personal accident policy will have only Accidental Death cover.

For detailed Term & Condition please refer Terms & Conditions tab.

|

Timing : 10 AM to 1 PM & 2 PM to 5 PM |

||||||

|

STATE |

CITY |

OFFICE Address |

CONTACT PERSON |

Contact Centre |

|

|

|

Maharashtra |

Mumbai |

11-C, Corporate Park,

|

Mr. Nitin Dharia |

022-41548300 |

||

|

Pune |

Office no. 12, C wing, Shreenath Plaza, F. C. Road, Shivaji Nagar, Pune-411004 |

Mr. Ashok Kasbe |

022-41548300 |

|||

|

Gujrat |

Ahmedabad |

437, B-wing , Advance Business Park , Opp: Swaminarayan Temple, Shahibaug, Ahmedabad-380004 |

Mr Arjun Dantani |

022-41548300 |

||

|

Vadodara |

Will operate from residence. |

Mr. Jaimin Gandhi |

022-41548300 |

|||

|

Surat |

316, Jolly Plaza, Near Navdi Bhandar, Athwa Gate, Surat - 395001 |

MR. Rinkesh Patel |

022-41548300 |

|||

|

Bengaluru |

25 Ashirwad, 4th B cross, 29th Main, 2nd stage, BTM Layout, Opp. Balaji Residency, Bangalore - 560076 |

Mr Bharath H N |

022-41548300 |

|||

|

Chennai |

1-G, No.22, Prince Arcade, Cathedral Rd, Gopalapuram, Chennai- 600086 |

Mr Vinoth |

022-41548300 |

|||

|

Kolkatta |

515, M.A Business Centre Pvt Ltd.5th Floor, Poddar Point, North Block, Park Street, Kolkata -700116 |

Mr Partha Sa |

||||

JAIN SWASTHYA BIMA YOJANA RENEWAL / NEW HEALTH PLAN (2022-2023 )

PARTNERS for JIO MEDICLAIM POLICY:

Insurance Company : Universal Sompo General insurance Co. Ltd.

TPA: Ericson Insurance TPA Pvt. Ltd.

Insurance Brokers: Gallagher Insurance Brokers Private Limited &

Synergy Insurance Broking Services Pvt. Ltd.

Policy Period: 20th April, 2022 to 31st March, 2023. Since you have paid after expiry of your policy on 31st March, 2022, during enrolment extension time, your cover shall start from 20th April, 2022 and No Claim Shall be allowed / considered if hospitalisation falling between 1st April, 2022 to 19th April, 2022. However, renewal member will get continuity benefit for hospitalisation after 20th April, 2022.

FAMILY FLOATER MEDICLAIM with Sum Insured options of Rs. 2 Lacs, Rs. 6 Lacs and Rs. 10 Lacs

1. FAMILY DEFINITION: Proposer + Spouse (Husband / Wife) + 4 Dependent children up to 25 years of age (Dependent & Unmarried) + 2 Parents OR In-Laws (Any 1 set of Parents to be covered. Combination not allowed) means Maximum 8 members allowed in one family (1+7)

2. INDIVIDUAL POLICY with Sum Insured of Rs.2 Lacs can only be opted by members who were covered last year under individual policy (Widow or widower) who do not have live spouse, children, parent or parent in law.

3. AGE LIMIT: 0-90 years (Entry Age of Proposer Between 18 to 90 Years), However ELDERLY MEMBERS who have already covered last year can continue in the Policy till LIFETIME

4. 1st year entry age is up to 90 years and upon renewal they can continue in the policy till LIFETIME

5. Any person cannot be covered in multiple family policy. If found enrolled in more than one policy, claim will be paid under one policy Sum Insured only during the whole year.

6. ROOM RENT & ICU CHARGES: Room Rent limitation Per Day will be capped as below:

|

Sum Insured |

Per Day Limit (Inclusive of Nursing, RMO, BMW, Infection control charges etc.) |

|

|

Normal Room |

ICU |

|

|

200,000 |

2,500 |

3,500 |

|

600,000 |

4000 |

6000 |

|

10,00,000 |

5,000 |

6,000 |

|

**IF THE INSURED OCCUPIES A ROOM WITH A ROOM RENT LIMIT OTHER THAN HIS ELIGIBILITY AS PER THE INSURANCE POLICY, THEN ALL THE OTHER CHARGES SHALL BE LIMITED TO THE CHARGES APPLICABLE FOR THE ELIGIBLE ROOM RENT OR ACTUALS, WHICHEVER IS LOWER** |

||

7. No addition or deletion of members are allowed during policy period, except for New born child in the family or newly married spouse, subject to intimation received in mail on jio. insurance@edelweissfin.com within 20 days of marriage or birth (for newly married SPOUSE & new born BABY) coverage will start from date of birth / Marriage. However, claim of New-Born Baby will be processed under reimbursement basis only.

Mid-term addition is not allowed in the policy. Any changes with relation to name, date of birth, age & sex of members informed after date of hospitalisation will not be corrected by Insurance Company. Hence any correction with regards to same has to be informed to jio.insurance@edelweissfin.com within 30 days of payment. Post loss corrections/ endorsement is also not allowed.

8. DAY CARE PROCEDURES: Day care procedures covered as per IRDA list.

9. All Internal congenital Diseases are covered

10. Compulsory deduction of Rs. 5000 will be applicable for each & every claim (applicable also in capped ailment listed below).

11. Domiciliary Hospitalisation, OPD treatment is not covered (Home quarantine not covered).

12. HOSPITALISATION AYUSH TREATMENT (AYURVEDIC / HOMEOPATHIC / UNANI): Treatment Covered subject to the treatment being taken in a Government hospital or in any institute recognized by Government and/or accredited by Quality Council of India or National Accreditation Board on Health.

13. Hospitalization arising out of PSYCHIATRIC AILMENTS Covered upto Rs.30,000

14. Cyber knife treatment: Covered with Co-pay of 50%

15. Cochlear Implant: Covered with Co-pay of 50%

16. Joint Replacement or Knee Replacement (including pre & post exp.) : covered subject to maximum one Joint Per family /per policy period for sum insured of Rs.2 Lakh & Rs.6 Lakh.

For Rs.10 Lakh Sum Insured both joints or bilateral Joint Treatment Per family /per policy period allowed.

1. 2 Lac Sum Insured: Rs. 75,000 per family per policy period.

2. 6 Lac Sum Insured: Rs 125,000 per family per policy period.

3. 10 Lac Sum Insured: Rs 150,000 per family per policy period.

#Note:

There will be ONE YEAR waiting period for Joint Replacement or Knee Replacement for New Members.

In case of ROAD TRAFFIC ACCIDENT the second joint replacement is covered. (Police FIR is MANDATORY) with above same capping.

17. Emergency Ambulance Charges: upto Rs.2,500 per hospitalisation.

18. TERRORISM: Covered from Day One

19. 30 Days Pre-Hospitalisation & 60 Days Post-Hospitalisation Expenses: Covered within Family Floater Sum Insured. Capping limit is including pre/post limit. Pre / Post claim is not allowed under Maternity claim.

20 MATERNITY BENEFIT : Maternity benefits, applicable only for the Member or Dependent Spouse, subject to a limit of Rs.30,000/- for normal and Rs.40,000/- for caesarean delivery up to 2 live children only. Maternity is not covered in individual policy. Pre / Post claim is not allowed under Maternity claim.

21 MATERNITY WAITING PERIOD : Waiting period of 9 months for maternity waived off for all existing renewal members; however waiting period of 9 months is applicable for new members enrolled under this policy. Maternity is not covered in individual policy.

22. NEW-BORN BABY COVER : Baby covered from Day 1 SUBJECT TO INTIMATION mail on jio.insurance@edelweissfin.com WITHIN 20 DAYS from Birth. However, claim of New-Born Baby will be processed under reimbursement basis only. To add name in policy, Submit New-born baby birth certificate issued by local government authority within 2 months from date of baby birth.

23. Pre & Post Natal Expenses: Covered on IPD Basis only and within Maternity limits. These Expenses are not covered on OPD Basis.

24. CO-PAYMENT:

|

Sum Insured |

Non Pre-Existing Diseases # |

Pre-Existing Diseases # |

|

200,000 |

NO-COPAY |

25% |

|

600,000 |

NO-COPAY |

25% |

|

1,000,000 |

NO-COPAY |

25% |

25 . # PRE-EXISTING DISEASES are covered from Day One subject to 25% Co-payment.( any disease which is incepted prior to 1st April 2022 shall be consider as PED and 25% Co-Pay shall get deducted)

26. Compulsory deduction of Rs. 5000 will be applicable for each & every claim (applicable also in capped ailment listed below).

27. 25% CO-PAY on all PRE-EXISTING DISEASE CLAIMS irrespective of age

28 Reimbursement Claims : Reimbursement of claims will be entertained. Subject to admission SHOULD BE intimated to TPA WITHIN 48 HOURS on jiointimation@ericsontpa.com and Toll free Number 18002022034 / 022-41548300 (If member fails to intimate to TPA within 48 Hours then the claim may be rejected).

29 DISEASE-WISE CAPPING ( 2022-2023 ) : This limit is overall limit, including Pre/post claim

|

Sum Insured |

2 Lacs |

6 Lacs |

10 Lacs |

|

Cataract (per eye) |

15,000 |

30,000 |

35,000 |

|

Cerebrovascular Accident including Brain related medical management and Surgery |

1,20,000 |

2,75,000 |

3,25,000 |

|

Cardiovascular Disease (Including Angiogram limit) |

1,20,000 |

2,75,000 |

3,25,000 |

|

Cancer |

1,20,000 |

2,75,000 |

3,25,000 |

|

Treatment for breakage of bone including spine surgery, Tendon & ligament repair / surgery |

1,20,000 |

2,20,000 |

2,80,000 |

|

Renal Complication (Including Dialysis limit) |

1,20,000 |

2,75,000 |

3,25,000 |

|

Genito Urinary / Calculus |

40,000 |

60,000 |

70,000 |

|

Dialysis |

35,000 |

45,000 |

50,000 |

|

Cholecystectomy including Medical Management |

40,000 |

60,000 |

70,000 |

|

Hysterectomy including salpingo-oophorectomy |

40,000 |

60,000 |

70,000 |

|

Appendectomy including Medical Management |

40,000 |

50,000 |

60,000 |

|

Fistula, Piles, Fissure |

30,000 |

40,000 |

50,000 |

|

Hernia overall limit (All types) |

30,000 |

40,000 |

50,000 |

|

Anaemia (Not for evaluation) |

50,000 |

50,000 |

50,000 |

|

Angiogram |

18,000 |

21,000 |

24,000 |

|

Joint and Knee Replacement |

75,000 |

1,25,000 |

1,50,000 |

|

maximum one Joint Per family /per policy period for sum insured of Rs.2 Lakh & Rs.6 Lakh.

For Rs.10 Lakh Sum Insured both joints or bilateral Joint Treatment Per family /per policy period allowed. |

* Compulsory deduction of Rs. 5000 will be applicable for each & every claim (applicable also in capped ailment listed above).

**Joint replacement capping will be applicable even if cause of Joint replacement is fracture.

30 SAMPLE CLAIM PROCESS FOR REFERENCE

i) If Claim is PED but not falling under any Sublimit ailment

In case of claim relating to PED; but not falling in any sublimit ailment. Say the hospital bill is Rs. 5 lakhs. (sum insured opted is Rs.10 lacs), the following procedure is adopted:

First the amount payable to the insured is worked out after adjusting the non-medicals and non-payables, room rent difference if any, proportionate deduction if the insured occupied a room with room rent more than his eligible amount.

|

Hospital bill |

Rs. 5.00 lakhs |

|

Deductions due to Non-payables |

- Rs. 2.00 lakhs |

|

Rs. 3.00 lakhs |

|

|

Deduct 25% Co-payment for PED |

- Rs. 75 Thousand |

|

Rs. 2.25 lakhs |

Since the diseases is not falling in any sublimit ailment; If on the contrary the assessed amount after co-pay is Rs.2,25,000/-Further Rs.5000/- will be deducted as mentioned above and hence final payable amount will be Rs.2,20,000/-.

ii) If Claim is Non-PED & Not Falling in any sublimit ailment:

In case of claim is not relating to PED & not falling in any sublimit ailment. Say the hospital bill is Rs. 5 lakhs. (sum insured opted is Rs.10 lacs), the following procedure is adopted:

First the amount payable to the insured is worked out after adjusting the non-medicals and non-payables, room rent difference if any, proportionate deduction if the insured occupied a room with room rent more than his eligible amount.

|

Hospital bill |

Rs. 5.00 lakhs |

|

Deductions due to Non-payables |

- Rs. 2.00 lakhs |

|

Rs. 3.00 lakhs |

Since the diseases is NON-PED & not falling in any sublimit ailment; the claim payable is Rs.3,00,000/-. Further Rs.5000/- will be deducted as mentioned above and hence final payable amount will be Rs.2,95,000/-.

31. For Corona Virus disease treatment if tested positive for corona virus at government approved lab. Home quarantine treatment is not covered.

32. ORGAN TRANSPLANT: The Insurance Company will pay expenses incurred on the Donor expenses for organ transplantation where the insured person is the recipient are payable provided the claim for transplantation is payable and subject to the availability of the sum insured. Donor screening expenses and post-donation complications of the donor are not payable. Donor expenses cover is subject to a limit of 10% of the Sum Insured or Rupees One lakh, whichever is less

33. DENTAL TREATMENT: covered if due to Road accident only and requiring 24 hours Hospitalisation. (FIR compulsory)

34. MID-TERM ADDITIONS allowed only for natural additionssubject to intimation received in mail on jio. insurance@edelweissfin.com within 20 days of marriage or birth (for newly married SPOUSE & new-born BABY) However claim of New-Born Baby will be processed only under reimbursement basis only. To add name in policy, Submit New born baby birth certificate & marriage certificate issued by local government authority within 2 month from date of baby birth or marriage.

Mid-term addition is not allowed in the policy. Any changes with relation to name, date of birth, age & sex of members informed after date of hospitalisation will not be corrected by Insurance Company. Hence any correction with regards to same has to be informed to jio.insurance@edelweissfin.com within 30 days of payment. Post loss corrections/ endorsement is also not allowed.

35. Any person cannot be covered in multiple family policy. If found enrolled in more than one policy, claim will be paid under one policy Sum Insured only during the whole year.

36. CLAIM INTIMATION in case of cashless claims, immediate intimation shall be given to jiointimation@ericsontpa.com or toll free number 18002022034/ 022-41548300 within 48 hours of Hospitalisation. In case of reimbursement claims, immediate intimation shall be given to Call Centre within 48 hours of Hospitalisation.

37. CLAIM SUBMISSION of documents for reimbursement claims Within 30 Days from Date of Discharge. Claim may get rejected due to delay submission.

38. In case of Road accident where FIR copy is provided, capping of Breakage of bone will not apply. For claims under accident Police FIR is compulsory.

39. Policy premium Details for Mediclaim Policy RENEWAL or NEW POLICY (2022 - 2023)

|

Family Size |

Sum Insured |

Premium Amount (With GST) 0-45 Y rs. |

Premium Amount (With GST) 46-60 Yrs. |

Premium Amount (With GST) 61-90 Yrs. |

|

Individual (only for Renewal members who had 2 Lac individual SI last year under same policy plan) |

Rs. 2 Lakh |

8,000 |

8,000 |

8,000 |

|

Family Floater of size 1+7 |

Rs. 2 Lakh |

15,000 |

20,000 |

30,200 |

|

Family Floater of size 1+7 |

Rs.6 Lakh |

21,000 |

30,000 |

44,500 |

|

Family Floater of size 1+7 |

Rs.10 Lakh |

30,000 |

38,000 |

63,300 |

PLEASE NOTE:

- Corona Virus disease treatment is covered under the policy as per Terms & Conditions.

- The above plan covers Personal Accident cover for Rs.5,00,000/- per person for each covered member of the family between the age of 18 years to 75 years of age only. So, in a family if there are 6 members than total Rs.30,00,000/- sum insured is available under the above plan. Nominee of the member will be spouse in case of married proposer's death and in case of unmarried proposer death, father or mother will be nominee.

- Member can increase the Sum Insured during renewal but can't decrease it.

- No Changes or cancellation are allowed in the policy once the payment is done.

- The policy premium will be paid directly by the member to USGIC account through payment gateway. USGIC will get consolidated premium through single remittance by the payment gateway. All the members will get Certificate of Insurance for the premium paid by him/her.

- Policy Premium can be PAID only via Online Payment. CHEQUE / NEFT / RTGS will not be accepted.

- Additional amount will be charged by payment gateway (PayU) for providing safe & secure online money transfer facility, which is addition to above Policy Premium charges. Payment gateway Convenience fees (+18% GST on Convenience Fees)

|

Payment Modes |

Convenience fees (GST extra) |

|

Debit Card (Visa, Master, Rupay, Maestro, etc.) Below 2000 Rs. |

Rs. 20 |

|

Debit card (Visa, Master, Rupay, Maestro, etc.) Above 2000 Rs. |

Rs. 20 |

|

Credit Card(Visa, Master, Rupay, Maestro, etc.) |

0.87 % |

|

Net Banking |

Rs 15 |

|

UPI (G-Tez, Phone Pe, etc.) |

Rs 15 |

- JIO JAC membership fees (non-refundable / non-transferable) for the financial year 22-23 is Rs. 1000 (GST extra). The same is additional to above Policy Premium. (Payment will get updated in next 1 week)

GST refund certificate will not be available under this policy however 80-D certificate under Income Tax will be provided in the name of proposer in the policy.

40. GENERAL EXCLUSIONS IN MEDICLAIM POLICY:

1. WAR like situation etc. :Treatment directly or indirectly arising from or consequent upon war or any act of war, invasion, act of foreign enemy, war like operations (whether war be declared or not or caused during service in the armed forces of any country), civil war, public defence, rebellion, uprising, revolution, insurrection, military or usurped acts, nuclear weapons / materials, chemical and biological weapons, ionizing radiation, contamination by radioactive material or radiation of any kind, nuclear fuel, nuclear waste.

2. SUICIDE attempt, CRIME etc.: An Insured Person committing or attempting to commit a breach of law with criminal intent, intentional self-Injury or attempted suicide while sane or insane.

3. Risky Sports, Military :Wilful or deliberate exposure to danger , intentional self-Injury, participation or involvement in naval, military or air force operation, circus personnel, racing in wheels or horseback, diving, aviation, scuba diving, parachuting, hang-gliding, rock or mountain climbing, bungee jumping, paragliding, parasailing, ballooning, skydiving, river rafting, polo, snow and ice sports in a professional or semi-professional nature.

4. Alcohol, Addiction etc.: Abuse or the consequences of the abuse of intoxicants or hallucinogenic substances such as intoxicating drugs and alcohol, including alcohol withdrawal, smoking cessation programs and the treatment of nicotine addiction or any other substance abuse treatment or services, or supplies, impairment of Insured Person's intellectual faculties by abuse of stimulants or depressants

5. Weight management programs or treatment in relation to the same including vitamins and tonics, treatment of obesity (including morbid obesity).

6. Correction of eyesight: Treatment for correction of eyesight due to refractive error including routine examination.

7. Health check-ups: All routine examinations and preventive health check-ups, including corona virus when hosptizalation is not done

8. Cosmetic surgery, aesthetic and re-shaping treatments and Surgeries. Plastic Surgery or cosmetic Surgery or treatments to change appearance unless medically necessary and certified by the attending Medical Practitioner for reconstruction following an Accident, cancer or burns.

9. Circumcision (unless necessitated by Illness or Injury and forming part of treatment); aesthetic or change-of-life treatments of any description such as sex transformation operations.

10. Hospitalisation not required: Conditions for which treatment could have been done on an outpatient basis without any Hospitalization.

11. Experimental treatment: Investigational treatments, Unproven / Experimental treatment , or drugs yet under trial, devices and pharmacological regimens.

12. Diagnostic Only: Diagnostic tests/procedures/treatment/consumables not related to Illness for which Hospitalization has been done.

13. REST CURE :Convalescence, cure, rest cure, sanatorium treatment, rehabilitation measures, private duty nursing, respite care, long-term nursing care or custodial care, treatment taken in a clinic, rest home, convalescent home for the addicted, detoxification centre, home for the aged, mentally disturbed remodelling clinic or any treatment taken in an establishment which is not a Hospital.

14. PREVENTIVE CARE/Vaccination including inoculation and immunizations (except in case of post-bite treatment); any physical, psychiatric or psychological examinations or testing.

15. Admission for enteral feedings (infusion formulas via a tube into the upper gastrointestinal tract) and other nutritional and electrolyte supplements unless certified to be required by the attending Medical Practitioner as a direct consequence of an otherwise covered claim.

16. Hearing aids & contact lenses or spectacles including optometric therapy, multifocal lens.

17. Baldness: Treatment for alopecia, baldness, wigs, or toupees, and all treatment related to the same.

18. Diabetic test strips etc.: Medical supplies including elastic stockings, diabetic test strips, and similar products.

19. External durable medical equipment: Any expenses incurred on prosthesis, corrective devices, external durable medical equipment of any kind, like wheelchairs crutches, instruments used in treatment of sleep-apnea syndrome or continuous ambulatory peritoneal dialysis (C.A.P.D.), devices used for ambulatory monitoring of blood pressure, blood sugar, glucometers, nebulizers and oxygen concentrator for bronchial asthma/ COPD conditions. Cost of artificial limbs, crutches or any other external appliance and/or device used for diagnosis or treatment (except when used intra-operatively). Sleep-apnea and other sleep disorders.

20. External Congenital Anomalies or diseases or defects.

21. Stem cell therapy etc. : Genetic disorders and stem cell implantation / Surgery, or growth hormone therapy.

22. Venereal disease, all sexually transmitted disease or Illness including but not limited to HPV, Genital Warts, Syphilis, Gonorrhoea, Genital Herpes, Chlamydia, Pubic Lice and Trichomoniasis.

23. "AIDS"(Acquired Immune Deficiency Syndrome) and/or infection with HIV (Human Immunodeficiency Virus) including Opportunistic infections but not limited to any conditions related to or arising out of HIV/AIDS such as ARC (AIDS Related Complex), Lymphomas in brain, Kaposi's sarcoma, tuberculosis, Pneumocystis Carinii Pneumoniae etc.

24. Voluntary termination, miscarriage (except as a result of an Accident or Illness)

25. Infertility: Treatment for sterility, infertility, sub-fertility or other related conditions and complications arising out of the same, assisted conception, surrogate or vicarious pregnancy, birth control, and similar procedures; contraceptive supplies or services including complications arising due to supplying services.

26. Organ donor screening: Expenses for organ donor

27. Illegal Organ Transplantation: Admission for Organ Transplant but not compliant under the Transplantation of Human Organs Act, 1994 (amended).

28. Spinal subluxation: Treatment and supplies for analysis and adjustments of spinal subluxation, diagnosis and treatment by manipulation of the skeletal structure; muscle stimulation by any means except treatment of fractures (excluding hairline fractures) and dislocations of the mandible and extremities.

29. Dental Treatment: Dentures, implants and artificial teeth, Dental Treatment and Surgery of any kind, unless requiring Hospitalization due to an Accident.

30. Cost incurred for any health check-up or for the purpose of issuance of medical certificates and examinations required for employment or travel or any other such purpose.

31. Artificial life maintenance including life support machine use, where such treatment will not result in recovery or restoration of the previous state of health.

32. Treatment for developmental problems , learning difficulties eg. Dyslexia, behavioural problems including attention deficit hyperactivity disorder (ADHD).

33. Treatment for Age Related Macular Degeneration (ARMD), Rotational Field Quantum Magnetic Resonance (RFQMR), External Counter Pulsation (ECP), Enhanced External Counter Pulsation (EECP), Hyperbaric Oxygen Therapy, high intensity focused ultrasound, balloon sinuplasty, Deep Brain Simulation,

34. Non-Medical Expenses (1):Expenses which are medically not necessary such as items of personal comfort and convenience including but not limited to television (if specifically charged), charges for access to telephone and telephone calls (if specifically charged), food stuffs (save for patient's diet), cosmetics, hygiene articles, body care products and bath additives, barber expenses, beauty service, guest service as well as similar incidental services and supplies, vitamins and tonics unless certified to be required by the attending Medical Practitioner as a direct consequence of an otherwise covered claim.

35. Treatment taken from a person not falling within the scope of definition of registered Medical Practitioner with any state medical council/ medical council of India.

36. Treatment charges or fees charged by any Medical Practitioner acting outside the scope of license or registration granted to him by any medical council.

37. Treatments rendered by a Medical Practitioner who is a member of the Insured Person's family or stays with him, except if pre- approved by Us.

38. Any treatment or part of a treatment that isnot of a reasonable charge, not medically necessary , drugs or treatments which are not supported by a prescription.

39. Non-Medical Expenses :(2) Administrative charges related to a Hospital stay not expressly mentioned as being covered, including but not limited to charges for admission, discharge, administration, registration, bio-medical, linen, documentation and filing, including MRD charges (medical records department charges).

40. Non-Medical Expenses :(3)including but not limited to RMO, CMO, DMO charges, Bio-Medical waste charges , Infection Control Charges etc. surcharges, night charges, service charges levied by the Hospital under any head are not payable because they are part of Nursing Charges and as specified in the Annexure for Non- Medical Expenses Click Here for more details

41. Treatment taken outside India

42. Insured Person whilst flying or taking part in aerial activities except as a fare-paying passenger in a regular scheduled airline or air charter company.

43. Robotic surgery (whether invasive or non-invasive) and Any form of Laser Surgery

44. All forms of Bariatric surgery.

45. Use of Radio Frequency (RF) probe for ablation or other procedure.

46. Admission primarily for diagnostic purposes not consistent with the treatment taken.

47. Blacklisted Hospital, Doctor: Treatment in any Hospital or by any Medical Practitioner or any other provider of services that We have blacklisted as listed on Our website.

48. Treatment provided by anyone with the same residence as Insured Person or who is a member of the Insured Person's immediate family.

49. Holmium Laser Enucleation of Prostate, KTP Laser Surgeries, Femto laser surgeries, bio-absorbable stents, bioabsorbable valves, bioabsorbable implants, oral chemotherapy, Hormonal Chemotherapy, Adjuvant Chemotherapy, Neo-adjuvant Chemotherapy, Immuno-therapy, use of Monoclonal antibody e.g. Trastuzumab , Antibody cocktail , Infliximab, rituximab, avastin, lucentis group of drugs.

50. Domiciliary Hospitalisation, OPD treatment is not covered (Home quarantine not covered).

51. Group Personal Accident (GPA) policy is also applicable for all the members covered under the family subject to age between 18 years to 75 years of age for only ACCIDENTAL DEATH cover (Police FIR Compulsory)

41. GENERAL EXCLUSIONS IN PERSONAL ACCIDENT POLICY:

1. Suicide/ Intentional self-injury

2. Death due to Pregnancy/childbirth etc.

3. Accident while under influence of alcohol/drugs

4. Sexually Transmitted Infections

5. Participation in a criminal act

6. Participation in a hazardous sport

7. War, civil war, surgical strike, similar situations etc

8. Other exclusion as per the Standard PA Policy

For more detailed exclusions, please refer standard Group Mediclaim Policy Conditions.

JAIN SWASTHYA BIMA YOJANA RENEWAL / NEW HEALTH PLAN (2022-2023 )

PARTNERS for JIO MEDICLAIM POLICY:

Insurance Company: Universal Sompo General insurance Co. Ltd.

TPA: Ericson Insurance TPA Pvt. Ltd.

Insurance Brokers: Gallagher Insurance Brokers Private Limited & Synergy Insurance Broking Services Pvt. Ltd.

MISUNDERSTANDINGS AND MYTHS OF JIO HEALTH PLAN

Will my policy divided in to 2 insurance company?

- NO

JIO is an Insurance Company?

- No. JIO is not an insurance company and does not give any type of insurance policy. JIO is the Group Manager of this policy. JIO has only played the role of negotiator for benefit of its Shravak/ Shravika Members

Who manages the Insurance Policy ?

The Policy is serviced by the following three entities:

Insurance Brokers (Like Prudent, Alliance, Almonds, Edelweiss, etc.) Insurance brokers are the mediators and communicator between JIO and Insurance Company to receive best terms. The responsibility of compiling the enrolment data, getting the policy endorsed, overview on claims process and resolving the queries of members is to be executed by the Insurance brokers. The Insurance brokers are the working hand of JIO for overall assistance for Group Policies.

Insurance Company (Like Govt. companies - National Insurance, Oriental Insurance & Pvt. Companies - ICICI Lombard, Star Health, Aditya Birla, Universal Sompo, etc.) The Mediclaim policy is issued by the government approved Insurance Companies under the regulation of IRDA. Means, the premium collected from members is transferred to the Insurance Company. The Insurance company bears the risks of the policy and pays claims to the members as per terms of the policy.

Third Party Administrators - TPA (Like Paramount, Vipul TPA, IL Health Care, Vidal, Health India, etc)

The TPA's are appointed by the Insurance Companies for issuing members Medi-claim card, communicate terms to policy holders, prepare panel of hospitals for cashless, receiving claim documents, evaluating the documents and sanctioning the claim amount.

Is JIO is making profits from the policies?

NO

JIO is not a profit making organization and is formed with a noble

objective of serving its Shravak / Shravika members as well as society at

large. Under the medical insurance scheme, the premiums are collected

individually from the members and then full amount is transferred as a

group premium to the insurance company. In-fact, Gurudev has inspired

several Jain Shravaks to donate partly towards the premiums for members of

their respective Samaj / Gnyati, who are financially troubled. Hence the

health security could be availed by members of their Samaj at further

discounted premiums. This will immensely help such families to face the

additional financial burden of medical expenses, if any.

Is the Enrolment process very complex?

NO

The enrolment process requires registering accurate details of the member

and their family so that they do not face any trouble during the full year

or at time of claim. The forms have been designed in a way to get the

important details only and no un-necessary details are to filled.

Whether any person are available for help during enrolment or at the time of claim like Insurance Agents ?

JIO has not appointed/authorized any retail agents for selling / marketing its policies. When the enrolment for policy is started, JIO chapters and volunteers across India assist in the policy and enrolment process and spreading information of policy. Because of the dedicated service of its volunteers, JIO has been able to reach huge number of Shravaks across India easily, without additional cost of hiring huge number of professionals.

And at the time of claim, members can take help / advice from helpline number of the insurance company. Alternatively, the members can also take help from any insurance agent because the process of claim is same as retail insurance policies.

Why so much importance is given to online process which may be difficult for a common man ?

JIO has pioneered in adopting to the latest technologies and online tool for your convenience and better service. The online enrolment process has the following major advantages:

The data entry and processing time is saved.

Accuracy of the data entered. This will also help in hassle free claims to the members.

Enrol anytime from anywhere

Immediate confirmation of enrolment completion.

Why JIO JAC number is compulsory?

JIO JAC is required not only for group Mediclaim but also for other JIO schemes. JIO introduced the Jain Advantage Card (JAC) as a comprehensive scheme for benefit of its members through bulk buying.

JIO JAC is a unique and permanent identification for availing benefits of various schemes launched by JIO. Members can easily participate in the programs of JIO without having to provide various details every time.

JAC members can also connect with fellow Shravaks and take full advantage of the JIO Global network.

Why does the policy coverage starts very late after payment of insurance premium to JIO?

JIO Group Policy is negotiated with Insurance Company for the Best TERMS and Lowest PREMIUM based on a commitment of certain Minimum NUMBERS of enrolment.

For enrolling the members, messages are sent to Shravaks residing all over India. An enrolment window period is kept open for members to fill forms and make premium payment.

In case the numbers fall short of the minimum target, then the enrolment period is extended for few days. After the closure of enrolment period, a list is compiled for all the forms received and payments are reconciled. Any errors found at the stage of validation and verification are corrected by contacting the members.

JIO pays the insurance premium to the Insurance Company through a single payment for all the members together for commencing policy. Upon payment, the Insurance cover period starts on common date for all the members. A single group policy document is issued in the name of JIO with the list of enrolled members and their families. On the basis of this TPA's issue Health Cards to all members with unique enrolment number for taking benefits of the policy.

The above process takes lot of time and efforts, hence the commencement of policy is after necessary period from the date of payment.

Why the Claims process is complex?

The process of filing claims for Cashless or Reimbursement with the Insurance Company is the same for JIO policy like any other retail mediclaim policies and in accordance with IRDA guidelines. In-fact, the norms for intimation of claim and the period for submitting claim documents after discharge are more beneficial in JIO Policy.

Whether insurance companies wrongly make huge deductions in JIO policy?

The deductions from claims are as per the terms of the policy and no ad-hoc deductions are made by the TPA or Insurance Company. The TPA and insurance company are bound by the guidelines of Insurance Regulatory & Development Authority.

However, in case any claims are wrongly deducted or disallowed, then the members can approach grievance department of Insurance company or Ombudsman department of IRDA. These actions are within the rights of every policy holder.

Whether JIO is responsible for answering queries on claims disbursal and deductions?

As clarified above, JIO is neither the Insurance Broker / Agent to the policy nor the company undertaking the insurance. JIO has played a role of Group Leader to the policy issuance. All the queries regarding the claims process, status of claims, reasons of deductions from claim etc., are handled by the concerned Insurance Company.

In cases, where the grievances of the policy members remain unresolved by the Insurance Company, the members can escalate such urgent / important issues with the Broking Company or JIO officials. JIO in turn will take up these issues with the concerned authorities through brokers. However the claims will be decided on merits of the case and within the terms of the policy.

Why has JIO not kept its word at the time of renewal by Increasing Insurance premiums and altering certain terms like amount capping on specific treatments and Co-pays on pre-existing diseases?

The 1st phase of policy saw an overwhelming response due to unbelievably low premiums and attractive benefits which are not available in any other policies. The biggest benefit of the policy was to cover elder members and members who were already ill. Due to such extra ordinary benefits, our Shravak families received a claim of almost 350% over the premiums paid. As a result of the heavy claim ratio, the renewal premiums were bound to be increased extensively by the Insurance Companies.

However it was necessary for JIO to keep the premium low and also provide suitable terms to members who have not lodged any claim. It is also necessary that group policy has a good share of healthy families to keep the claim ratio balanced along-with affordable premiums year after year. This will help to serve more number of needy and sick people with stable premium year after year. Accordingly JIO had renegotiated the terms of policy with insurance company and achieved a group policy with balanced terms and appropriate premiums which were still better than the market rates.

The JIO Mediclaim policy still continues to be hugely beneficial to the middle class families and the senior citizens who otherwise were not able to take benefit out of medical insurance.

Why do Insurance Companies, brokers or TPA change at time of each renewal?

Each phase of policy had been negotiated with different insurance companies and the Best offer with maximum benefits and lowest premiums has been selected. The brokers and TPA change accordingly.

When do the new phase are introduced and how will the Shravaks be informed about the same?

The introduction of new phases is not as per a planned schedule. JIO receives proposals from different insurance companies and if JIO is convinced about the suitability of the terms, the new phase will be announced through SMS, e-mails and website to all JIO JAC members.

Why there are no proper contact details for call or email for filing grievances? Why No one answers the call or proper answers are not received from helpline?

The responsibility for coordination of enrolment and claims has been assigned to the brokers by JIO. The brokers are required to maintain appropriate number of contact points in the form of helpline numbers and email id for helping members and resolving their queries.

For any help or assistance at the time of enrolment the members can contact the brokers helpline numbers -.Toll Free Number : 180030103360

jiointimation@ericsontpa.com & Toll Free No :18002022034 / 022-41548300

Whether the policy is a temporary affair or will continue for several years to come?

The JIO group policy is NOT a temporary affair and will continue in future like all other insurance policies.

However, as discussed earlier, the terms of the policies and the premiums are subject to change at the time of each renewal based on previous year experience & analysis.

JIO group Mediclaim policy was started with a noble vision of giving financial security in medical emergency to all the Shravak / Shravika families. Therefore JIO will never think about discontinuing the scheme.

How is the premium calculated for group policy?

If a group policy is issued for the first time then the general claim ratio of individual policies is considered. Further the fact that the company receives huge number of policy holders at one time, the reduced advertisement costs can be passed on by way of discount on premium.

For renewal of group policy, the premiums are decided on the basis of past claim ratio, age composition of the policy holders, types of claims made earlier and assumptions made for future claims.

What are the changes in the revised terms of policy?

Most of the policy benefits of earlier JIO Mediclaim policy have been retained.

Any person cannot be covered in multiple family policy. If found enrolled in more than one family, claim will be paid on anyone family floater policy only during whole year.

Compulsory deduction of Rs. 5000 will be applicable for each & every claim.

What is the procedure for renewal?

A member is required to visit the designated website for renewal and login with JIO JAC ID. The details of proposer, family members will be reflected for last year Existing Members Only. The member is required to confirm the complete details before proceeding. The member can also read the detailed terms and conditions of the new policy. On acceptance of the terms of the policy the member can make payment of premium and complete the process.

Whether Physical Submission of forms is allowed?

Physical forms will not be accepted at all for the renewal of policy. All the information has to be provided online.

What are the options for making payment of premium amount?

The members can choose to make payment of premium amount only from following options

Online payment through credit / debit card or net banking

Payment gateway Convenience fees

|

Payment Modes |

Convenience fees (GST extra) |

|

Debit Card (Visa, Master, Rupay, Maestro, etc.) |

Rs. 20 |

|

Debit card (Visa, Master, Rupay, Maestro, etc.) Above 2000 Rs. |

Rs. 20 |

|

Credit Card(Visa, Master, Rupay, Maestro, etc.) |

0.87 % |

|

Net Banking |

Rs 15 |

|

UPI (G-Tez, Phone Pe, etc.) |

Rs 15 |

If a member is not aware about the online process or the working on internet and computers, how will they be able to renew?

In this age of digitization, internet and computer facility is easily available. The members who are not very conversant with use of computers are advised to approach young members in their family for help in completing the online process.

- TERMS, CONDITIONS & PROCEDURE for this New Plan

Can I opt individual policy in JIO Mediclaim Renewals?

Yes, Only if you had individual policy previous year under the same plan.

Can I opt Family Floater policy in JIO Mediclaim Renewals?

Yes.

This is an insurance scheme where a family can opt for an insurance plan for Rs.2, 6 & 10 Lac against Mediclaim for Self + Spouse + 4 Unmarried, Dependent Children up to 25 years of Age and Parents or parents in-laws (Jain only) this policy includes personal accident cover for a sum of Rs.10 Lac for Proposer.

I am a Jain but my wife is not a Jain? Can I insure my wife?

Under the family floater policy you can cover your wife as long as the proposer is Jain and because now she is a part of the Jain family. All covered members has to be Jain.

If I have only 3 members in my family can I buy a Family Floater Policy?

Family Floater Policy is available for family size ranging between 2 to 8 members i.e. Proposer + Spouse + 4 Unmarried, Dependent Children up to 25 years of Age + Parents/or Parents or Laws (jain only) up to 90 years

Can I and my brother / sister cover our parents under our individual family floater schemes?

Yes you can but any person can't be covered more than once under whole group in JIO Policy. If declared more than once, benefit would be payable under one Sum Insured only

We are two brothers & we have two different policies, Can we enrol our Parents in both policies?

No. One person can be covered only once in a JIO policy.

Can I take my married daughter in policy?

No. As she is now not part of your family.

Is this Applicable on Pan India basis?

Yes this policy is for Pan India, Jain population only. All covered members has to be Jain.

What if I am or my family member is already suffering from a disease? Can I yet get myself or my family members covered?

Pre-Existing Diseases are covered since day 1, however Co-pay of 25% will be applicable for PRE-EXISTING Ailments.

In my family few are having Jain certificate but my parents don't have any proof? Then what I can do?

Please get a confirmation from your Sangh / Gyati that you are a Jain.

What are the major changes in the revised terms of policy?

Co-pay of 25% will be applicable for Pre-existing Ailments / Diseases

No co- pay will applied on Non-PED Cases for Sum Insured of 2 Lacs, 6 Lacs & 10 Lacs

Compulsory deduction of Rs. 5000 will be applicable for each & every claim (applicable also in capped ailment listed above).

Reason for including this deductible of Rs 5000 in this policy ?

As we are aware that the JIO Mediclaim Policy is now in its 8th Year. In the past there was huge claim ratio in JIO policy. To Adjust (recover) the additional burden of high claims, the Insurance Company increases the insurance premium every year at the time of renewal.

There was a considerable hike in the JIO Insurance Premium in the previous year. Gurudev and JIO Directors have decided that there should not be any major increase in the renewal premium this year.

To compensate the Insurance Company and make the policy viable considering the high claim ratio, it is decided to introduce additional deduction of Rs. 5000/- on claim.

What is the name of Insurance Company?

Universal Sompo General Insurance Co.Ltd

Is Addition / corrections allowed in policy ?

Mid-term addition is not allowed in the policy. Any changes with relation to name, date of birth, age & sex of members informed after date of hospitalisation will not be corrected by Insurance Company. Hence any correction with regards to same has to be informed to jio.insurance@edelweissfin.com within 5 days of payment. Post loss corrections/ endorsement is also not allowed.

How do I renew?

Please follow the below mentioned steps

Please go on www.jio.net.in/R22-23.php

Read revise Terms & Conditions carefully

Select "Apply Now"

Enter JIOJAC ID

Fill your enrolment details

Make payment ONLINE

Can I submit physical form?

You can't submit Physical Form. The process of enrolment and payment is online only through JIO website.

What are the options for making payment I am not aware of online procedure?

You need to Enrol Online only, however payment can be done via Online through Easebuzz after completing Online Enrolment Procedure.

If I don't have JIO JAC Id, can I opt for Mediclaim Policy ?

No, JIOJAC ID is compulsory for proposer. Please register online for JIOJAC ID.

What is the premium?

Premium details are available in Salient features section.

Does this scheme have cashless as well as Reimbursement facility?

Yes, cashless facility is available in 6000 Network of hospitals and Member can avail Cashless as well as reimbursement facility. In all case of cashless claims, immediate intimation shall be given to our Call Centre within 48 hours of Hospitalisation. In case of reimbursement claims, immediate intimation shall be given to Call Centre within 48 hours of Hospitalisation.

When will I be eligible for my maternity claim?

For Existing Members, Maternity Benefit is covered from Day 1 up to 2 live children only. However for New Members, Maternity benefit is available after completion of 9 months from the date of enrolment in JIO - Shravak Arogyam scheme. This benefit is not available for Individual Policy Holder with 2 Lakh Individual sum insured.

Are pre & post-natal expenses under Maternity benefits covered?

Pre & Post Natal expenses on OPD/IPD bases are not covered

What shall be the next year premium?

The next year premium will be decided after the end of the policy tenure based on the Claim Experience of the current Policy

Can I have the policy number?

No, you will not get Policy Number. However you will receive Cover Certificate and Health ID card, which you can show in Network Hospitals to avail Cashless Benefit under this Policy.

Do we get no claim bonus if we do not claim in the existing year?

No, as this is a Group scheme you will not get NO Claim Bonus

If my wife is the proposer can she cover her parents?

Yes, only if she is a Jain by birth.

How different is TPA from Insurance Company?

Third Party Administrator (TPA) in Health Insurance Sector servicing all insurance companies. Health Insurance policies for individuals are basic products of Insurance Companies on which TPA adds value and facilitates smooth operation through its value-addition like network of healthcare service providers, medical care standardization, Claims management, Client servicing, expert opinion etc. Thus TPA administers a `healthcare package' for its clients with customized healthcare delivery.

Will location of dependent family matter in availing services under TPA?

No, Location does not affect the operational activities, main member or the dependent member can avail same and equal benefits irrespective of their location. TPA Network of Healthcare Service Providers is across the country. These accredited healthcare providers would assure qualitative healthcare delivery to TPA members.

Will the change in names in between policy period matters?

Yes, According to the Insurance Company the claim will not be settled (unless prior intimation to Insurance company) if there is any alterations in the name, It has to be intimated to your respective Insurance Co. within 15 days on receipt of your cards & requisite Endorsement for the change in name needs to be passed by Insurance co. This has to be done first hand and not only if any claim arises.

Corona Virus Cover

Treatment of COVID-19 is covered under this policy. even though it will be declared as Epidemic and/or Pandemic. Home quarantine treatment is not covered.

What are the documents required to be submitted to TPA to claim under reimbursement procedure?

Documents that you need to submit for a hospitalization reimbursement claim are:

Original completely filled in Claim form

Covering letter stating your complete address, contact numbers and email address (if available), along with Schedule of Expenses

Copy of the TPA ID card or current policy cover certificate copy and previous years' policy copies (if any)

Original Discharge Card/ Summary

Original hospital final bill

Original numbered receipts for payments made to the hospital

Complete breakup of the hospital bill

All bills for investigations done with the respective Doctor

All bills for medicines supported by relevant prescriptions

Bank Details with Cancel Cheque

You are advised to keep Photo Copy of the entire set of claim documents submitted to us.

TPA or Insurance Company may ask for additional documents (apart from the list shared) as required during the claim process

How to send reimbursement claims?

Under this Policy, You can avail Reimbursement facility and claims can be submitted to Ericson Insurance TPA Pvt. Ltd office at 11-C, Corporate Park, S. T. Road, Chembur, Mumbai - 400071, Maharashtra. through registered post / courier.

What are "NON-MEDICAL EXPENSES"?

Your health insurance policy pays for reasonable and necessary medical expenditure. There are several items that do not classify as medical expenses during hospitalization. These items will not be payable and expenditure towards such items will have to be borne by you.

Can I claim medical expenses incurred before and after a surgery?

You can claim medical expenses incurred 30 days before and 60 days after hospitalization (as specified in your policy), provided they are related to the ailment/treatment for which you were hospitalized. Such expenses are termed as pre and post hospitalization, except for Maternity Claims.

Can I claim my dentist's bills?

No. You can do so only in cases arising from Road Accidents requiring hospitalisation. (Police FIR Compulsory)

Are all the tests prescribed by the doctor at a hospital reimbursed under the Health Insurance Plan?

Expenses incurred at a hospital or a nursing home for diagnostic purposes such as X-rays, blood analysis, ECG, etc. will be reimbursed if they are consistent with or incidental to the diagnosis and treatment of the ailment for which the policy holder has been hospitalized. In any other scenario, these expenses will not be reimbursed.

Will my claims be reimbursed even if I do not get myself treated at a network hospital?

Yes, you can avail Reimbursement facility.

Is there a minimum time limit for stay within the hospital under the health insurance plan?

Typically, the insured can make a claim if her/his hospitalized stay is for over 24 hours. However, for certain treatments, such as dialysis,

chemotherapy, eye surgery, etc. the stay could be less than 24 hours. Day care claims will be processed as per IRDA rule.

What happens when the limit of insurance is exhausted under a Health Insurance Policy?

If the insurance limit i.e. the sum insured is exhausted in a particular year due to large medical expenses, the insurer is not liable to bear/reimburse the insured for any further expenses.

Who will receive the claim amount if the proposer dies at the time of treatment?

The insurance company will insist upon a succession certificate from a court of law for disbursing the claim amount. Alternatively, the insurers can deposit the claim amount in the court for disbursement to the legal heirs of the deceased.

What is the procedure for availing cashless facility?

In case of planned hospitalization, insurers require the first prescription with the details of the case history indicating following details:

Provisional diagnosis or reason for getting admitted in hospital

Proposed date of admission

Approximate expenses

Name of the hospital and consultants

Approximate duration of stay at the hospital

Attached doctor's prescription with admission note

The above documents need to be delivered to the TPA/insurer at least 72 hours before admission.

If I avail of the cashless facility, will the insurance company pay the entire bill at the hospital?

No. From the Bill amount, Non-Medical Expenses will be deduced and if any, Co-pay, sub limits & Deductible is applicable that will be deducted. Also if the Room Rent limit is more than the eligible limits as per the respective Sum Insured, then all other eligible Medical Expenses will be paid in proportion to eligible Room Rent Category. And the balance amount will have to be borne by the insured if any.

Further Premium FOR Mediclaim & Personal Accident for all family members with wellness pack is inclusive of GST

What are Sub-limits in this policy?

This limit is overall limit, including Pre/post claim

|

Sum Insured |

2 Lacs |

6 Lacs |

10 Lacs |

|

Cataract (per eye) |

15,000 |

30,000 |

35,000 |

|

Cerebrovascular Accident including Brain related medical management and Surgery |

1,20,000 |

2,75,000 |

3,25,000 |

|

Cardiovascular Disease (Including Angiogram limit) |

1,20,000 |

2,75,000 |

3,25,000 |

|

Cancer |

1,20,000 |

2,75,000 |

3,25,000 |

|

Treatment for breakage of bone including spine surgery, Tendon & ligament repair / surgery |

1,20,000 |

2,20,000 |

2,80,000 |

|

Renal Complication (Including Dialysis limit) |

1,20,000 |

2,75,000 |

3,25,000 |

|

Genito Urinary / Calculus |

40,000 |

60,000 |

70,000 |

|

Dialysis |

35,000 |

45,000 |

50,000 |

|

Cholecystectomy including Medical Management |

40,000 |

60,000 |

70,000 |

|

Hysterectomy including salpingo-oophorectomy |

40,000 |

60,000 |

70,000 |

|

Appendectomy including Medical Management |

40,000 |

50,000 |

60,000 |

|

Fistula, Piles, Fissure |

30,000 |

40,000 |

50,000 |

|

Hernia overall limit (All types) |

30,000 |

40,000 |

50,000 |

|

Anaemia (Not for evaluation) |

50,000 |

50,000 |

50,000 |

|

Angiogram |

18,000 |

21,000 |

24,000 |

|

Joint and Knee Replacement |

75,000 |

1,25,000 |

1,50,000 |

|

maximum one Joint Per family /per policy period for sum insured of Rs.2 Lakh & Rs.6 Lakh.

For Rs.10 Lakh Sum Insured both joints or bilateral Joint Treatment Per family /per policy period allowed. |

* Compulsory deduction of Rs. 5000 will be applicable for each & every claim (applicable also in capped ailment listed above).

**Joint replacement capping will be applicable even if cause of Joint replacement is fracture.

Sample claim process

(I) If Claim is PED but not falling under any Sublimit ailment

- In case of claim relating to PED; but not falling in any sublimit ailment. Say the hospital bill is Rs. 5 lakhs. (sum insured opted is Rs.10 lacs), the following procedure is adopted :

- First the amount payable to the insured is worked out after adjusting the non-medicals and non-payables, room rent difference if any, proportionate deduction if the insured occupied a room with room rent more than his eligible amount.

|

Hospital bill |

Rs. 5.00 lakhs |

|

Deductions due to Non-payables |

Rs. 2.00 lakhs |

|

Rs. 3.00 lakhs |

|

|

Deduct 25% Co-payment for PED |

Rs. 75 Thousand |

|

Rs. 2.25 lakhs |

Since the diseases is not falling in any sublimit ailment; If on the contrary the assessed amount after co-pay is Rs.2,25,000/-, the claim payable is Rs.2,25,000/-. Further Rs.5000/- will be deducted as mentioned above and hence final payable amount will be Rs.2,20,000

(II) If Claim is Non- PED & Not Falling in any sublimit ailment:

- In case of claim is not relating to PED & not falling in any sublimit ailment. Say the hospital bill is Rs. 5 lakhs. (sum insured opted is Rs.10 lacs), the following procedure is adopted :

- First the amount payable to the insured is worked out after adjusting the non-medicals and non-payables, room rent difference if any, proportionate deduction if the insured occupied a room with room rent more than his eligible amount.

|

Hospital bill |

Rs. 5.00 lakhs |

|

Deductions due to Non-payables |

Rs. 2.00 lakhs |

|

Rs. 3.00 lakhs |

Since the diseases is NON-PED & not falling in any sublimit ailment; the claim payable is Rs.3,00,000/-. Further Rs.5000/- will be deducted as mentioned above and hence final payable amount will be Rs.2,95,000/-.

Deductible of Rs. 5000 is applicable in each claim.

What happens in case of an Emergency hospitalization where Cashless facility is not authorized to me?

jiointimation@ericsontpa.com & toll free no.18002022034 / 022-41548300

How a hospital is defined with regards to the health insurance policies?

Any institution established for indoor care and treatment of sickness and/or injuries, which is duly registered and supervised actively by a registered medical practitioner.

OR

Any establishment that satisfies the following criteria can qualify as a

hospital:

- with at least 15 patient beds

- With a fully equipped operation theatre of its own if surgical procedures need to be carried out

- Employing fully qualified nursing staff around the clock

- Having fully qualified doctors in charge around the clock Note: For Class 'C' towns, the number of beds relaxed to ten.

What is meant by hospitalization?

An instance where the insured individual is hospitalized for a minimum period of 24 hours can be termed as hospitalization. Specific treatments like dialysis, chemotherapy, radiotherapy, laser eye surgery, dental surgery, etc. when the patient is discharged on the same day are also considered hospitalization under day care as per IRDA guidelines.

Is maternity benefit available under an individual Health Insurance Plan?

No. Maternity benefit is not payable under Individual Health Insurance Plan.

What is my room rent eligibility under both the schemes?

|

Sum Insured |

Per Day Limit (Inclusive of Nursing, RMO, BMW, Infection control charges etc.) |

|

|

Normal Room |

ICU |

|

|

200,000 |

2,500 |

3,500 |

|

600,000 |

4000 |

6000 |

|

10,00,000 |

5,000 |

6,000 |

|

**IF THE INSURED OCCUPIES A ROOM WITH A ROOM RENT LIMIT OTHER THAN HIS ELIGIBILITY AS PER THE INSURANCE POLICY, THEN ALL THE OTHER CHARGES SHALL BE LIMITED TO THE CHARGES APPLICABLE FOR THE ELIGIBLE ROOM RENT OR ACTUALS, WHICHEVER IS LOWER** |

||

What are the age limit restrictions under both the policies?

. In case of Family Floater below age limit will apply

- For Unmarried, Dependent Children maximum age allowed is 25 years. After completion of 25 years, Child will not be covered in next year

- For Parents / parents in law (jain only) maximum entry age is 90 years, Renewal till LIFETIME

Can one prepare a Jain Certificate?

The Jain certification has to be from Gyati / Samaj / Sang only

What is covered under Personal accident Cover?

Death Benefit is covered under personal accident cover (Police FIR Compulsory)

What claim documents do I need under a Personal Accident Claim?

CLAIM DOCUMENTS REQUIRED FOR PERSONAL ACCIDENT CLAIM - ALL DOCUMENTS HAVE TO BE DULY ATTESTED / CERTIFIED / NOTARIZED

- Compete Filled Claim Form

- Photocopy Of ID Proof

- Death Certificate

- Post Mortem Report

- Police FIR Copy Compulsory.

- Driving license (if self -driving)

- Police Panchnama Copy